In the matter of materiality, the new reporting trends have put forth two perspectives:

- financial materiality, which indicates that a topic is material if it has significant impact on the organisation’s financial performance;

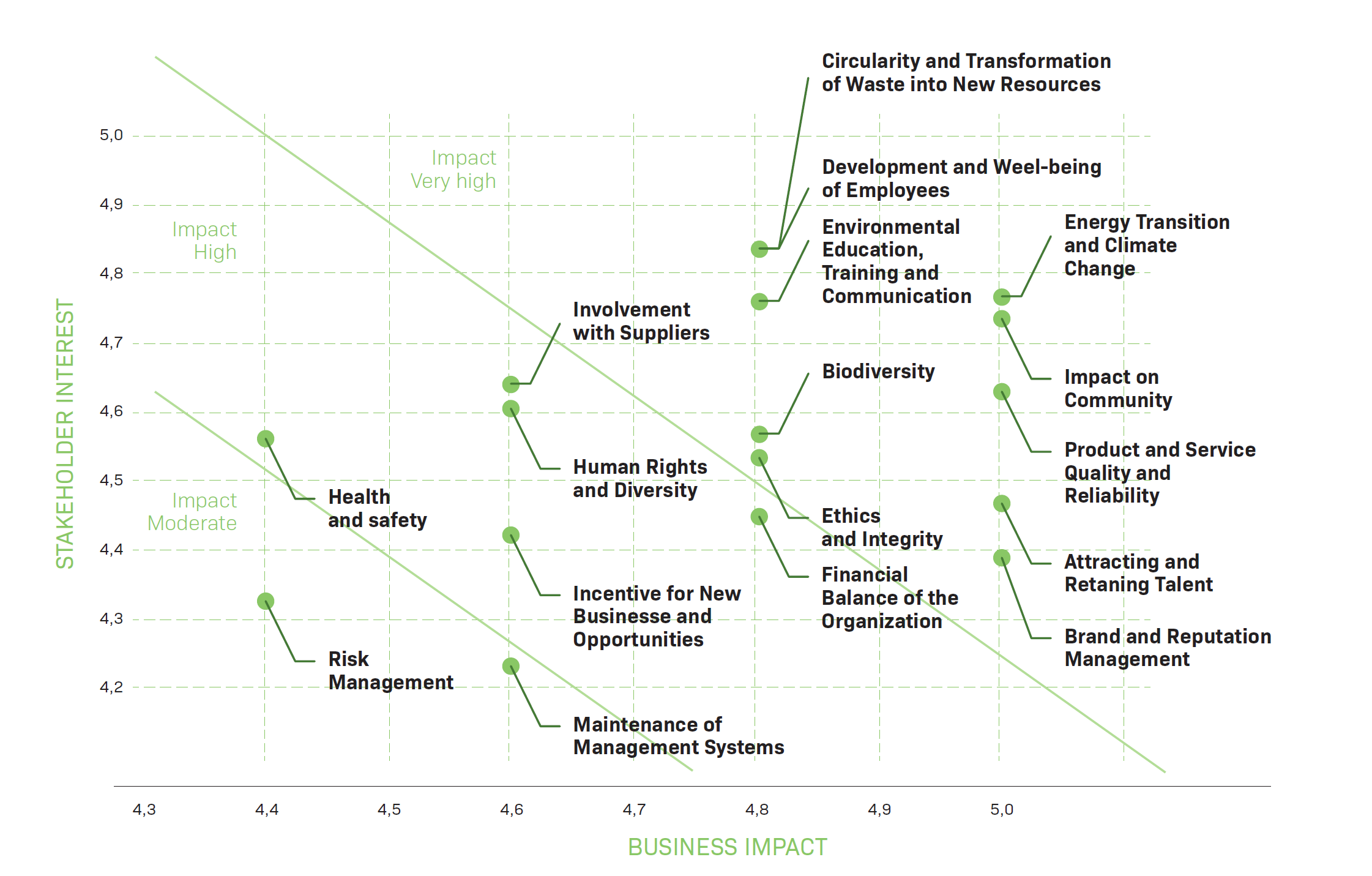

- social and environmental materiality, when the topic is materially relevant if the activities have a significant impact on society. In this context, the European Commission has consolidated these two perspectives by introducing the concept of "Double Materiality”.

In the course of the materiality review process carried out in 2022, LIPOR based its analysis on and aligned its activities with the concept of double materiality, believing that it adds value to the Organisation and its Interested Parties.

- Share

-

-

-

-